The world economy was already in trouble before the US and Israel attack on Iran commencing February 2026. Writing in May, the nature of the conflict may well have changed by the time these words are read. In any event, however, the restrictions so far on shipping through the Straits of Hormuz will have effects on the world economy. The war will accelerate a world-wide economic crisis that will inevitably mean attacks on workers and suffering among the peoples of the Global South.

Marxist economist Michael Roberts has noted (in a blog titled “Shortages, Inflation and Stagnation”, 3 May 2026) the projections of the World Bank:

The World Bank released its latest Commodities Outlook report and it makes alarming reading for the world economy, especially for the poorest countries and their people. Energy prices are projected to surge by 24% this year to their highest level since Russia’s invasion of Ukraine in 2022. Overall commodity prices are forecast to rise 16% in 2026, driven by soaring energy and fertilizer prices and record-high prices for several key metals.

Indermit Gill, the World Bank Group’s Chief Economist concluded that: “the war is hitting the global economy in cumulative waves: first through higher energy prices, then higher food prices, and finally, higher inflation, which will push up interest rates and make debt even more expensive,” He went further: “The poorest people, who spend the highest share of their income on food and fuels, will be hit the hardest, as will developing economies already struggling under heavy debt burdens. All of this is a reminder of a stark truth: war is development in reverse.”

Roberts points out that stagflation, stagnation and inflation at the same time:

had already been emerging well before the Iran conflict broke out. The war has only accelerated that process – the major economies are like a pair of scissors; the bottom blade (growth) is dropping further while the upper blade (prices) is rising faster – so the gap between the blades is widening.

Major central banks are in a dilemma on whether to raise or cut interest rates. Under neoliberal economic dogma, hiking interest rates should depress the economy and squeeze out inflation; however, the imposition of higher interest rates runs the risk of tipping already fragile economies into a full-scale slump. On the other hand, a reduction in interest rates would tend to boost the economy, but at the cost of higher inflation.

Roberts says that:

US consumer inflation (PCE index) reached 3.6% yoy in April. PCE inflation has been moving up relentlessly for the past 10 months, and the energy price spike will now add to that in future months. So even the US is facing stagflation. Prices are rising in the US in part due the self-inflicted wounds of Trump’s tariffs.

On 21 May 2026 the European Commission released its Spring 2026 Economic Forecast. They say that EU growth is projected to slow to 1.1 percent in 2026, down from 1.5 percent in 2025. In the narrower and economically stronger euro area the growth forecast for 2026 is even worse: 0.9 percent.

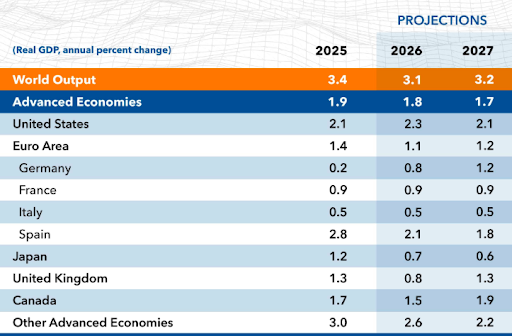

The global slow down is most marked in the advanced economies. The table below is from the IMF’s World Economic Outlook (April 2026). It shows that Germany, France, Italy, Japan, and the UK are all expected to register less than a one percent increase in GDP in 2026.

China is a different story. According to the IMF’s World Economic Outlook (April 2026), inflation is still very low. Growth is trending down, currently at 4.4 percent a year. Sluggish demand has seen the unemployment rate rise to 5.1 percent.

Since this article is written for Aotearoa readers, here are some latest economic statistics for this country provided by Stats New Zealand. The Consumer Prices Index (inflation) has risen incrementally since September 2024 and stands at 3.1 percent according to the latest data. Wages are rising by just 2.0 percent a year. The unemployment rate is 5.3 percent. GDP growth of 0.2 percent in 2025 means the economy has barely been moving. These statistics are comparable with those of the mainstream of Western developed economies.

Another element of the developing crisis of world capitalism is public debt, the subject of an article featured on the front page of the International Monetary Fund’s website. The authors say that public finances were already stretched before the war on Iran: “Even when economies recovered, fiscal positions did not. Global growth was robust in 2025, yet there was no meaningful progress in repairing budgets. In many countries, deficits stayed high, debt kept rising, and interest bills grew rapidly.” Governments are spending more and more on servicing debt.

Into this equation comes a global rise in military spending. Notably, the US has succeeded in bullying other NATO members into increasing their military budgets. Unless these states can increase their incomes through economic growth and taxation, the costs of more military spending can only come from cuts in other departments of government or from more debt. New Zealand did not need to be bullied. In 2025 Luxon’s coalition government was only too keen to launch a massive increase in military spending under a Defence Capability Plan. In line with this commitment, the government announced a $1.58 billion increase for the New Zealand Defence Force in the May 2026 Budget.

Periodic economic crises are inevitable under capitalism. It is equally inevitable that ruling classes will seek to resolve crises at the expense of working classes. We know both of these things from historical experience, and we know it from Marxist theory. Marx discovered that the cause of economic crises was the tendency of the rate of profit to fall leading to slow investment and production of goods. Capitalists, of course, do not like diminishing profits, even though that’s an inherent feature of the system they uphold. Marx says that to counteract or avert the falling rate of profit, the capitalist class takes measures to offset the tendency of the rate of profit to fall. The two most important of these are to increase the intensity of exploitation and to depress wages. Increased work intensity is exactly what we have experienced in the neoliberal era from the 1980s. There is nothing inevitable about the capitalists succeeding in their increased exploitation of workers. Workers can and do fight back. The question has to be asked, though, why unionised workers in many developed countries have failed to prevent the employers’ attacks? But that is another story.

In conclusion, if major economies of the world continue on the current downward path, we can expect an invigorated, world-wide employers’ offensive against workers’ conditions as the capitalists seek to restore profit margins. Indeed, in Aotearoa, increasing attacks on the working class are already taking place across the board.

Branner Image: World map made from assorted coins, symbolising global finance. Image credit: Monstera Production on Pexels.